- AI in Insurance Industry

- 2026-06-24

AI in Insurance Industry: Use Cases, Benefits, Costs & Future Trends

Audio Track

Table of Contents

Key Takeaways

- AI in insurance is reshaping fraud detection, underwriting, customer engagement, and claims processing by enhancing speed, accuracy, and operational efficiency across the value chain.

- Structured, high-quality, and governed data is important for unlocking business value from use cases of AI in insurance and ensuring trustworthy and compliant decision-making.

- Insurers who start with high-impact, focused use cases like predictive analytics or claims automation can achieve speedy ROI via cost reduction, enhanced loss ratios, and improved customer retention.

- AI is shifting the insurance industry, starting from a reactive “detect and repair” model to a proactive “predict and prevent” strategy approach, using real-time behavioral data and real-time insights.

- Insurers are investing in regulatory alignment, ethical AI, skilled talent, and scalable infrastructure that will result in the next wave of innovation in the AI-powered insurance industry.

Overview: AI Insurance and How It Works

AI in insurance refers to utilizing advanced algorithms and ML models for automating processes, analyzing large amounts of data, and offering actionable insights. These technologies allow insurers to enhance multiple aspects of their operations, from claims and underwriting to customer service and fraud detection.

AI in insurance means harnessing data-driven insights and automating processes to improve efficiency, decrease costs, and enhance customer satisfaction. At present, 87% of surveyed insurers are already seeing their companies investing $5 million or more in AI technology every year. 47% of insurance executive have the plan of increasing their investment in AI.

As AI technologies are continuously evolving, their effect on the insurance industry is going to grow, resulting in more unique and innovative solutions and a better overall experience for the policyholders and the insurers. To avail the benefits of AI in your insurance business, you will have to partner with a professional AI app development company.

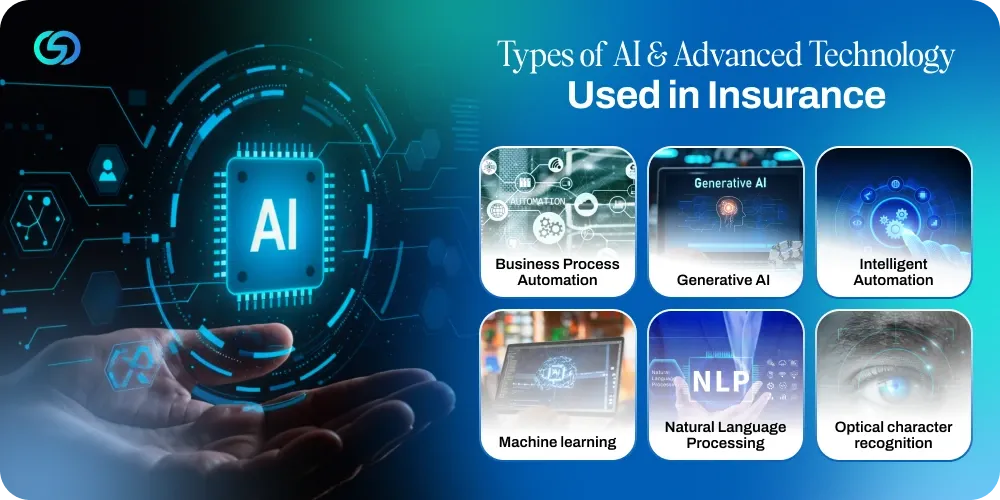

Types of AI & Advanced Technology Used in Insurance

There are multiple AI models that insurance companies can use to enhance their operations. The various types of AI in insurance are as follows:

➡️ Business Process Automation

Business process automation (BPA) helps in automating complex and repetitive business processes in insurance. BPA can seamlessly handle customer onboarding, underwriting, claims processing, and other policy management services.

➡️ Generative AI

Generative AI utilizes large language models (LLMs) and can help insurance businesses in several ways. Gen AI can help insurance employees optimize tasks like answering customer service problems as well as analyzing documents or individual text blocks. Generative AI can help the customer service representatives to respond in a better way to the problems of the customers. It can also help the customers of the insurance companies with their own problems by using AI technologies like virtual assistants and chatbots.

➡️ Intelligent Automation

Intelligent automation can be described as the hallmark of any AI-driven workflow. It includes using automation technologies for optimizing and scaling decision-making across businesses. For instance, an insurance provider utilizes intelligent automation for calculating payments, addressing compliance needs, and estimating rates.

➡️ Machine learning

Machine learning utilizes data and algorithms to allow AI to imitate the way humans learn, while improving accuracy gradually. Insurance businesses can utilize Machine Learning technologies like deep learning for analyzing their customer information and providing services that make product recommendations to prospects and customers.

➡️ Natural Language Processing

Natural language processing, or NLP, is an AI category that leverages machine learning to allow computers to understand and communicate with human language. Insurance providers can utilize NLP to parse the data that customers supply for finding out whether they can provide the right insurance and at what cost. For instance, businesses offering healthcare insurance can ask prospects questions about their medical histories to better underwrite their insurance offerings.

➡️ Optical character recognition

Optical character recognition (OCR), also known as text recognition, utilizes automated data extraction for converting images to text faster into a machine-readable format. It is a critical component for insurance businesses’ approach to digitizing, converting legacy assets into searchable digital content. Utilizing OCR for digitizing old forms and claims for putting into a database can help them in understanding the complete history of their business and service offerings better.

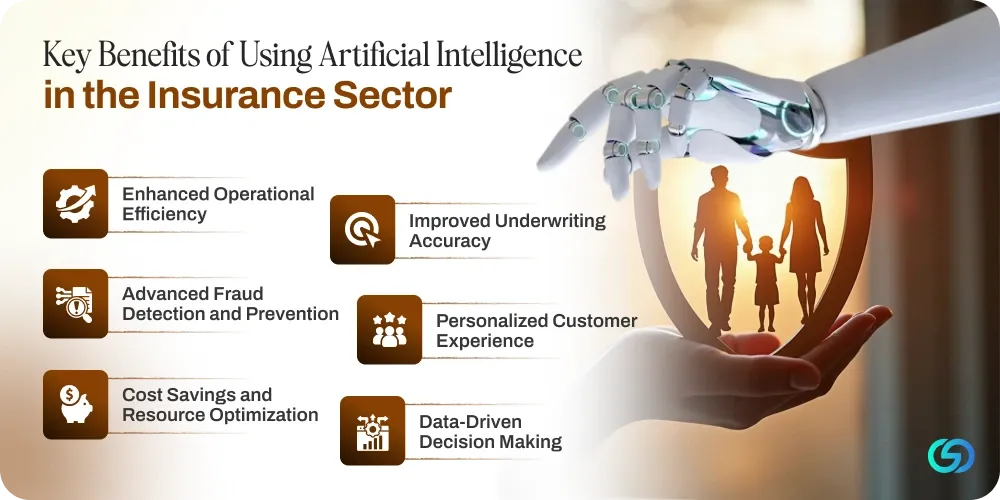

Key Benefits of Using Artificial Intelligence in the Insurance Sector

AI is powering transformative value across the insurance industry by improving operational efficiency, decreasing costs, and enhancing customer experiences. This allows insurers to compete effectively and provide faster and smarter services.

⏺️ Enhanced Operational Efficiency

AI automates repetitive and time-consuming tasks such as data entry, claims settlement, and underwriting, allowing insurers to process high volumes of work faster and with fewer errors, which boosts overall productivity.

⏺️ Improved Underwriting Accuracy

Machine learning models analyze huge datasets for assessing risks with greater precision, helping insurers set more accurate premiums and make data-driven underwriting decisions that decrease loss exposure.

⏺️ Advanced Fraud Detection and Prevention

AI systems find out suspicious anomalies and patterns in claims data, allowing fast detection of fraudulent activities and a major reduction in fraudulent payouts, safeguarding both insurers and honest policyholders.

⏺️ Personalized Customer Experience

AI-powered chatbots and virtual assistants provide customized support around the clock while data analytics allow customized recommendations of products, enhancing engagement, convenience, and customer satisfaction.

⏺️ Cost Savings and Resource Optimization

By decreasing manual workloads and optimizing workflows, AI lowers the costs of operations. These savings can be reinvested into the main business operations or passed on to customers via competitive pricing.

⏺️ Data-Driven Decision Making

AI helps in unlocking actionable insights from big data. This empowers insurers to make strategic decisions in areas such as risk management, pricing, and market trends. This helps in strengthening long-term business performance.

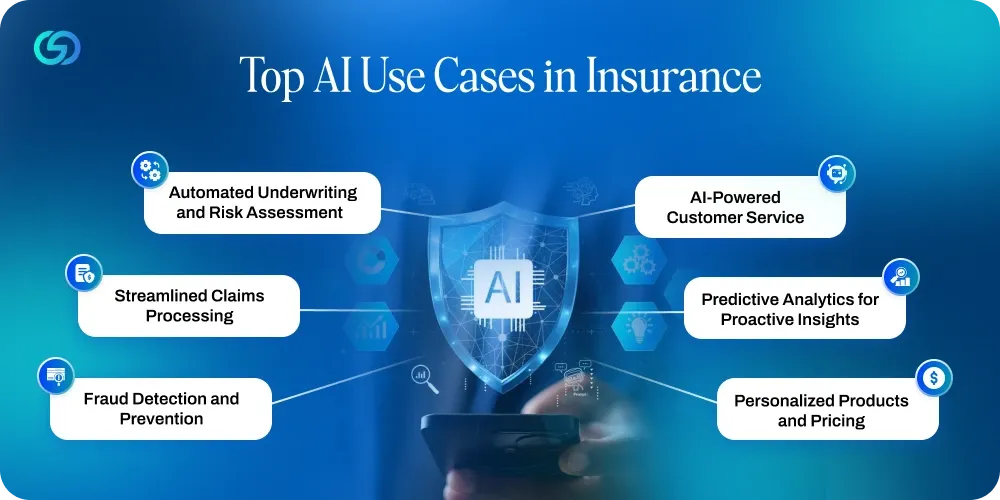

Top AI Use Cases in Insurance

AI technologies are now being adopted across insurance businesses for automating processes, enhancing accuracy, and providing more customer-centric services. Starting from risk evaluation to handling of claims, these practical use cases demonstrate how AI is revolutionizing insurance operations and results.

🔶 Automated Underwriting and Risk Assessment

AI models analyze large volumes of unstructured and structured data, including historical claims, customer profiles, and external data sources, for assessing risk more quickly and accurately. This results in faster underwriting decisions and more precise pricing for policies.

🔶 Streamlined Claims Processing

AI tools like computer vision, OCR, and natural language processing automate document review, eligibility checks, and damage evaluation. This decreases manual workload, shortens processing times, and improves consistency via the lifecycle of claims.

🔶 Fraud Detection and Prevention

Machine learning algorithms help in detecting unusual anomalies and patterns in submission claims, helping insurers to findout and flag potential fraud in real time. This helps in protecting revenue and enhances overall risk control.

🔶 AI-Powered Customer Service

Conversational AI, including virtual assistants and chatbots, provides 24/7 support for onboarding, policy inquiries, claims updates, and more. These tools enhance responsiveness, decrease call centre loads, and improve customer satisfaction.

🔶 Predictive Analytics for Proactive Insights

AI-driven predictive analytics helps insurers in forecasting customer behaviour, potential risks, and future claims trends. These insights support personalized offers, proactive outreach, and strategic decision-making.

🔶 Personalized Products and Pricing

By utilizing AI for analyzing individual risk profiles and lifestyle information, insurers can develop customized insurance products and dynamic pricing models that align well with customer requirements, enhancing relevance and competitiveness.

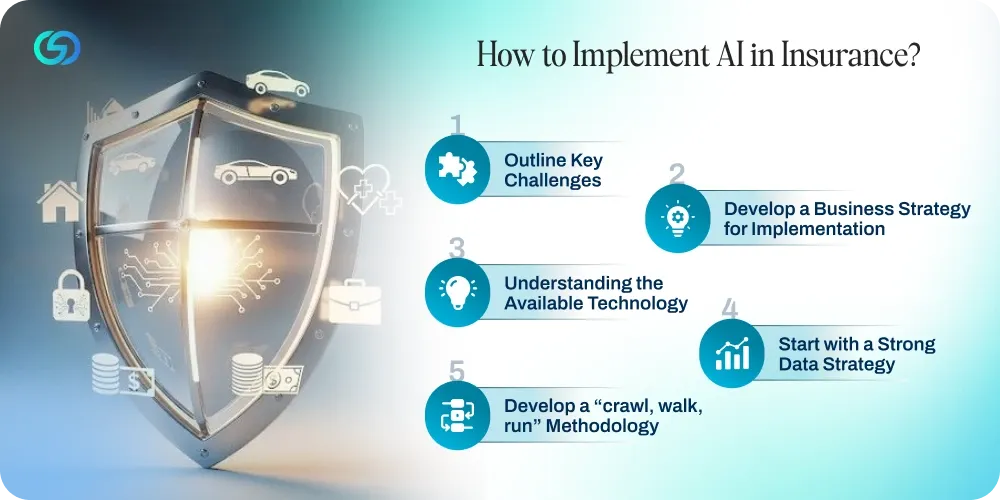

How to Implement AI in Insurance?

When businesses implement AI, it is crucial to follow a framework based around AI strategy. By developing an AI solution incrementally, your business can design AI that helps in serving specific objectives. Given below are the following steps throughout the process of implementation:

▶️ Outline Key Challenges

What are the challenges your company is facing? Are these issues claims-related, growth against other insurance players, or top-line growth?

▶️ Develop a Business Strategy for Implementation

What do you particularly need for accomplishing with an AI solution, and how are you going to measure its success? What are the important performance indicators you are intending to monitor? Who is accountable for the success of the program?

▶️ Understanding the Available Technology

What are the current and best AI-related technologies addressing business challenges and strategies? Understanding the available and most used challenges helps you determine the which technology will help meetings your needs.

▶️ Start with a Strong Data Strategy

Before getting into developing a solution, consider the information you already have available and any data collection you may require performing. Understand the quantity, type, and data quality that you have. In case you do not have robust in-house data science or AI expertise in-house, consider working with a reliable third-party to help determine and execute your data strategy.

▶️ Develop a “crawl, walk, run” Methodology

Start small by addressing a particular challenge or customer requirement when developing an AI solution. Then move faster and conduct short-term tests on multiple solutions utilizing proof of concept implementations. From there, you can broaden your mission by incorporating additional use cases and aligning with business priorities.

How is AI Enhancing Customer Engagement and Service Delivery?

AI technology is mainly transforming how insurance businesses interact with customers, from initial policy shopping to claim settlement and beyond. The applications of AI mostly deliver the maximum visible advantages, directly affecting customer satisfaction, retention, and acquisition. Leading insurance companies are utilizing AI for developing responsive, customized, and proactive customer experiences that separate them in the competitive markets.

1️⃣ Virtual Assistants and AI-Driven Customer Service

Virtual assistants driven by gen AI have turned ubiquitous in customer service operations in insurance companies. The AI tools offer basic advice, address common inquiries, and handle full routine transactions without human intervention. Modern virtual assistants understand natural language, easily escalate complicated issues to the representative of customer service when necessary, and maintain context across conversations.

The availability of AI-powered customer service 24/7 represents a significant enhancement over traditional call center operations. Customers can get instant answers to the questions related to coverage, request ID cards, make policy changes, and file claims at any hour without any hold. This kind of convenience is specifically valuable during stressful situations such as property damage or accidents when customers require immediate assistance.

Gen AI chatbots excel at managing high volumes of simultaneous customer interactions, something which is not possible for human representatives. During significant catastrophic events such as wildfires or hurricanes generating thousands of claims simultaneously, AI systems guide customers via immediate next steps, triage inquiries, and gather preliminary claim information. This capability helps in preventing customer service operations from becoming overwhelmed during crisis periods.

The balance between human touch and AI automation remains crucial for the satisfaction of customers. Insurance businesses are learning that some interactions still need judgment, empathy, and problem-solving capabilities that can only be provided by human representatives. The most effective customer service operations utilize AI for handling routine queries efficiently while ensuring seamless handoffs to customer service representatives for situations that need human judgment.

2️⃣ Personalization Via AI Applications

Beyond handling the inquiries of the customers, AI systems allow unprecedented personalization in the products and services of insurance. A 160-year-old US-based insurance business underwent an important digital transformation to offer more personalized financial services experiences to its millions of customers and 10,000 advisors across multiple touchpoints. By utilizing a unified platform in its customer-friendly solutions to aggregate behavioural and transactional data along with the main attributes, the company offers business users the best recommendations for easy customer engagement.

AI-driven customization helps insurance businesses move beyond the generic policy offerings towards completely individualized insurance products. Usage-based insurance programs' premiums depended on the exact driving behaviour, home security measures, or activity levels, which rely on AI systems for processing real-time information from the mobile telematics providers, as well as calculating the proper adjustments in pricing.

Insurance businesses utilizing advanced personalization tools report increases in engagement by 37% and enhancements in conversion rate by 45% via personalized campaigns. These customized programs appeal to low-risk customers who benefit from lower premiums while offering insurers deeper customer relationships and better risk data that decrease churn and enhance lifetime value.

Predictive insights from AI allow proactive engagement of customers that helps in preventing losses, rather than only compensating for them. Insurers can alert the homeowners about potential risks of property to weather patterns, remind the drivers about maintenance schedules that suggest health interventions that decrease medical claims, or prevent mechanical failures. This shift from reactive claim payment to proactive management of risk develops value for both insurance companies and customers.

The customer engagement advantages of AI personalization extend allover the policy lifecycle. Starting from initial quotes reflecting individual circumstances, via policy administration that anticipates the needs of the customer, to processing claims that account for personal preferences, AI allows consistently customized experiences that develop customer loyalty and decrease churn.

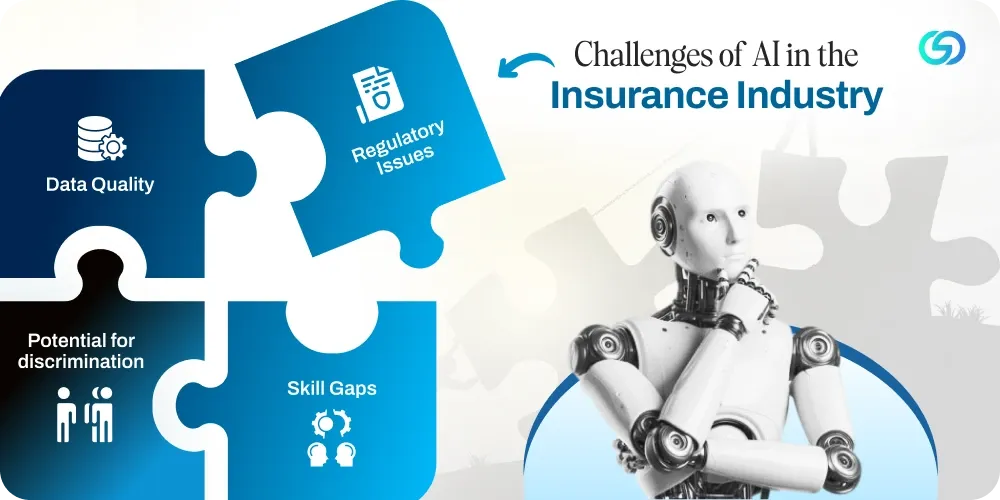

Challenges of AI in the Insurance Industry

Integrating AI in insurance poses potential risks, which businesses must anticipate. The various challenges of AI in insurance are as follows:

🔷 Data Quality

Utilizing AI can result in some data issues. The technology is still evolving, so making mistakes is possible, like hallucinating information that is not there or making wrong assumptions about a request. An insertion of phantom data can have a major effect on strategic decisions that arise from the data. This helps in reinforcing the requirement to utilize employees for checking the results that are produced by AI or use other types of checks and balances.

🔷 Potential for discrimination

Since AI is trained on human data sets, AI models are capable of indiscriminating, either refusing to provide insurance to overcharging premiums or specific groups. There may be some regulatory concerns in businesses that do not take adequate set for curtailing any potential problems with discrimination. Thus, insurance businesses should not be utilizing generic generative AI tools such as ChatGPT and should either work with businesses that develop specific tools or develop their own tools.

🔷 Regulatory Issues

Insurance carriers should be taking steps to safeguard customer data. AI can help in protecting that information, but using external AI tools could be a violation of specific regulations. Insurance carriers must deeply investigate any AI tools that they are considering and seek guidance from legal professionals before exposing any customer information to those technologies.

🔷 Skill Gaps

Businesses in the insurance industry may not have the correct resources internally to take complete advantage of AI. The current employees may not have the right skills. Similar to other industries, the insurance business must invest in AI upskilling and reskilling to prepare those employed for jobs in the future, jobs with AI as a main component. It should also hire new employees who are already skilled in AI.

Measuring AI Impact and Business Value

Quantifying the ROI of AI is a challenge for lots of insurance businesses, yet measuring the business value of AI in insurance is important to justify the continued investments in AI and guide the allocation of resources. Top insurers have developed comprehensive frameworks to assess the impact of AI across customer satisfaction, operational efficiency, competitive positioning dimensions, and risk management.

↗️ Claims Accuracy and Processing Speed

Improvement tracking in AI in insurance claims, like decreased processing times and rates of error. This helps in quantifying operational gains. Accurate and faster claims handling directly improves customer satisfaction and reduces administrative costs.

↗️ Cost Reduction and Efficiency Gains

Measuring policy administration expenses, reductions in annual labour, and fraud-related losses helps in demonstrating how AI streamlines resources. Quantifying these cost savings provides a powerful indicator of the economic value of AI to the business.

↗️ Customer Experiences Metrics

Monitoring retention rates, customer satisfaction scores, and digital engagement levels reflects how AI affects service delivery. Improved personalization, responsiveness, and easy interactions reflect measurable enhancements in customer experience.

↗️ Risk Prediction Accuracy

Evaluating predictive models’ precision in finding risk patterns and forecasting loss trends enables insurers to determine the effectiveness of AI-driven risk assessments. Improved prediction supports enhanced pricing and underwriting decisions.

↗️ Revenue Growth and New Opportunities

Tracking the impact of revenue from AI-powered offerings like personalized products or proactive cross-selling. This helps in demonstrating AI innovation’s business value. Growth in new customer segments and sales shows successful adoption.

↗️ Compliance and Risk Management Outcomes

Measuring how AI in insurance supports regulatory compliance, decreases risk exposure, and improves audit transparency helps insurers determine broader business benefits. Enhancements in these areas signal robust governance and operational resilience.

What are the Cost Implications of Implementing AI in Insurance?

Implementing AI in insurance includes important initial investments in technology infrastructure, talent acquisition, and software development. Insurers should allocate funds for buying or developing AI systems, incorporating them with the already present processes, and training staff to leverage the new tools effectively.

Moreover, before introducing AI, a business should first prepare the data and processes that will power the AI, mainly by means of harmonization and data standardization. Or else, there is a risk that it will be exposed to incorrect results and so-called AI hallucinations.

However, these upfront expenses can be offset by increased efficiency and long-term savings. AI decreases operational expenses by automating routine operations, improving fraud detection, speeding up claims processing, and leading to smaller losses and enhanced risk management.

Moreover, AI-powered personalization can improve customer satisfaction and retention, potentially enhancing revenue. All over, while the initial financial expenditure is substantial, the ROI via cost savings and growth in revenue can be crucial.

What Future Trends are Emerging with AI in the Insurance Industry?

The adoption of AI in the insurance industry is speeding up, with next-generation technologies revamping processes, products, and customer experiences. The emerging trends point towards deeper personalization, smarter automation, and more predictive decision-making that will define insurance’s future.

➡️ AI-Driven Predictive and Prescriptive Analytics

Future AI systems are going to move beyond descriptive insights to prescriptive and predictive analytics, anticipating the needs of the customer, forecasting loss patterns, and recommending optimal actions for pricing and risk mitigation.

➡️ Explainable and Ethical AI Models

As customer expectations and regulations grow, insurers will be increasingly adopting explainable AI that offers transparency into decision logic, develops trust in automated results, and supports compliance.

➡️ Improved Personalization Via Behavioural Data

AI will utilize richer behavioural datasets like IoT device readings or real-time usage patterns to provide hyper-personalized coverage, pricing, and engagement customized to risk profiles and individual risk profiles.

➡️ Real-time Risk Monitoring and Adaptive Pricing

Insurers will utilize AI for monitoring risks in real-time, starting from driving behaviours to health metrics, allowing adaptive pricing models that reward safe patterns and proactively adjust coverage.

➡️ Conversational and Multimodal AI Interfaces

Chatbots and voice assistants will emerge with multimodal capabilities, allowing easy interactions across voice, text, and visual inputs. These AI agents will handle onboarding, complicated inquiries, and claims support more intuitively.

How can Insurers Prepare for AI Changes?

Insurance companies can prepare for AI changes by embracing a dual approach of regulation and innovation.

Firstly, investing in AI technologies like ML algorithms can improve the efficiency of claims processing, improve underwriting accuracy, and personalize customer service. This includes developing strong data strategies for ensuring that the AI models are trained on quality data and updated regularly to stay relevant.

Secondly, adapting to regulatory frameworks is critical to ensure implementation of AI complies with data protection laws and insurance standards, thereby fostering transparency and trust with policyholders.

Incorporating a human-in-the-loop element further assures that AI decisions are monitored continuously and validated by experienced professionals, adding an added layer of oversight and accountability.

By fostering a collaboration and continuous learning culture between data scientists, AI experts, and regulatory professionals, we can effectively harness the transformative potential of AI while navigating the regulatory challenges.

Conclusion

AI in insurance is not an emerging concept but a strategic need. Starting from underwriting and fraud detection to AI in insurance claims and personalized engagement of customers, AI use cases in insurance are providing measurable accuracy, efficiency, and growth of revenue. Insurance companies that invest in robust data foundations, ethical AI frameworks, and scalable implementation strategies are getting a competitive edge in a largely digital market. While challenges like data quality, compliance, and skill gaps remain, the long-term value far outweighs the risks. As AI technologies are continuously evolving, the insurance sector will shift from reactive claim management to preventive and predictive risk intelligence, reshaping how insurers develop value for stakeholders and policyholders.

FAQ

Is AI going to replace claims adjusters?

AI is not expected to completely replace the claim adjusters but rather change their roles by automating routine tasks as well as acting as a digital assistant. While AI helps in handling the extraction of data, routine settlements, and damage detection, claim adjusters remain important for empathy, complex negotiations, and nuanced decision-making.

In what capacity is AI currently being used in Insurance?

AI at present is being used in the insurance industry as a main operational technology enhance accuracy, efficiency, and personalization across the complete value chain, converting it from a ‘detect and repair’ model to a ‘predict and prevent approach. It is highly utilized in claims management, fraud detection, underwriting, and customer service, with AI adoption rates that drive a 35.1% CAGR in the sector between 2024 and 2029.

What is the top AI-powered tools used in the insurance industry?

AI-powered tools in the insurance sector are revolutionizing operations by automating manual tasks, improving risk assessment accuracy, and enhancing customer experience. Main applications in 2026 involve AI-powered underwriting, AI in insurance claims processing, and fraud detection.

How can AI improve claims processing for auto insurance companies?

AI enhances auto insurance processes by allowing faster, more accurate, and automated workflows, decreasing resolution times from weeks to hours and minutes. By leveraging computer vision AI, which analyzes photos of vehicle damage for estimating repair costs, while ML algorithms detect fraud, automate data entry, improve customer experience, and organize fraud rings.

How does AI improve fraud detection in property insurance?

AI enhances fraud detection in property insurance by replacing slow, rule-based, manual processes with advanced analytics that work in real-time for predicting and preventing fraudulent activity. By utilizing machine learning, computer vision, and natural language processes, insurers are capable of analyzing huge amounts of data for detecting anomalies, inconsistencies, and patterns that manual reviews miss.

Where can I find AI-based customer service chatbots for insurance providers?

Insurance service providers can adopt AI chatbots via enterprise AI platforms or partner with specialized development companies. For customized, secure, and scalable chatbot solutions designed mainly for insurance workflows, you can choose ConvexSol for developing intelligent, completely integrated customer service automation systems.

How does AI improve loss ratio management in insurance companies?

AI enhances the management of loss ratio for insurance businesses by streamlining risk selection, automating the processing of claims, and improving fraud detection. By utilizing predictive analytics and ML, AI allows more precise, individualized underwriting pricing and finds high-risk claims early, which decreases unnecessary operational costs and payouts, finally enhancing complete profitability.

What internal data readiness is required before implementing AI in insurance?

Implementing AI in the insurance sector needs to transform fragmented, legacy system information into a high-quality, centralized, and governed asset. The main requirement is “AI-ready” data that is structured, clean, and accessible information that powers ML models for delivering unbiased, reliable, and compliant insights.

How can legacy insurance systems integrate with AI solutions?

Integrating legacy insurance systems with AI solutions includes a phased, strategic approach that layers advanced technology over the existing infrastructure, rather than replacing it immediately. The goal is to bridge rigid, outdated systems with flexible AI models for enhancing data accessibility and customer experience.

How soon can insurers expect ROI from AI investments?

Insurers can expect to see measurable ROI from investing in AI within 6 to 12 months for high-impact, targeted use cases. However, major enterprise-wide transformation with complex agentic AI systems can take up to 2 to 4 years to provide complete, satisfactory returns.

Can small and mid-sized insurers afford AI adoption?

Yes, small and mid-sized insurance companies can afford AI adoption, and in several cases, they cannot afford to ignore it. While large businesses largely invest in proprietary systems, small insurance companies can utilize affordable, third-party AI solutions, SaaS apps, and targeted pilot projects for achieving competitive gains without huge upfront costs. In fact, most of the mid-sized businesses that are investing in AI see operational cost reductions within their first year.