- Enterprise Software Development for BFSI

- 2026-06-06

Enterprise Software Development for BFSI: Security-First Architecture

Audio Track

Table of Contents

Key Takeaways:

- Security-first architecture safeguards BFSI systems from compliance failures, cyber threats, and customer distrust.

- Modern BFSI software balances real-time transactions, secure integrations, and ensures zero tolerance for downtime.

- AI, automation, and RPA support financial institutions in detecting fraud faster and strengthening the overall operations.

Why Security-First Matters in BFSI?

Trust is everything in financial services.

Say, a customer taps “pay now,” checks insurance claims or applies for a loan and expects the transaction to happen in real-time and securely. It may appear simple on the surface, but it is a complex digital ecosystem on the inside. This is why BFSI software development has become a priority for modern financial institutions.

Banks, fintech firms, insurers, and lenders manage personal data, money, and digital transactions, which makes the BFSI sector vulnerable to cyberattacks across the world. A single breach can lead to customer distrust and major operational disruption.

For quite a long time, several businesses followed a pattern where the platform was built first, and security was added later. However, in BFSI, that approach doesn’t hold up anymore. Security needs to be integrated at the architecture level.

The enterprise systems running today are more seamlessly connected than ever before. Regulations like KYC, AML, PCI-DSS, and GDPR are shaping financial platforms, making it crucial to be monitored and maintained.

This is the reason why BFSI businesses are slowly turning towards a fintech software development company to build secure foundations because in modern systems, security needs to be a part of the architecture right from the first day.

What Is Enterprise Software Development in BFSI?

BFSI stands for Banking, Finance Services, and Insurance, specializing in developing digital platforms, systems, and applications for the industry. Spanning from modern banking systems and lending solutions to digital insurance and wealth management systems, each is designed around strict security and regulatory requirements.

The global BFSI enterprise software market size reached $16.52 billion in 2025 and is projected to achieve $100.23 billion by 2035.

So, when people hear “enterprise software” in financial services, it is much bigger than reality.

▶️ Core BFSI Enterprise Systems

The core banking system manages the central operations of a bank, including accounts, withdrawals, deposits, and customer records.

▶️ Payment Systems

From UPI transfers to card payments, payment gateways, and digital wallets, these platforms process money securely and quickly.

▶️ Lending Platforms

Enterprise software development for banking automates loan origination, disbursement, underwriting, and collections by integrating with the KYC system and credit bureaus.

▶️ Fraud Detection Systems

Financial systems depend on intelligent systems to spot suspicious activities, reduce fraud, and flag anomalies.

▶️ Customer Portals

Customer portals provide secure self-service banking across mobile and web, requiring strong authentication, encryption, and smooth UX.

What makes enterprise banking software different from software in most other industries?

- High transaction volumes: An advanced financial platform may process over thousands of transactions every day without performance degradation.

- Real-time processing: Customers don’t have to wait for balances to update or payments to clear. Transactions must happen accurately and without delay.

- Regulatory compliance: Every action and every data movement need to meet compliance requirements such as AML, KYC, and PCI-DSS.

- Zero tolerance for downtime: Even a short amount of unavailability can trigger significant financial loss.

These make BFSI systems uniquely demanding.

Why Security-First Architecture Is Non-Negotiable in BFSI

BFSI software does more than merely support operations. It moves money, connects several financial systems, and stores sensitive customer information. All of it helps in decision-making that happens in real-time.

A financial platform’s security vulnerability can expose account information. A delay in a retail app may frustrate users. Both can damage trust that requires years to develop.

This is exactly why a security-first architecture matters.

Key Risks in BFSI Systems

➡️ Data Breaches

BFSI companies store volumes of data related to account numbers, credit scores, transaction histories, and so on. This makes them a high-value target for attacking.

Compared to other industries, in case of a data breach leads to a compounding impact. Beyond the financial loss, institutions need to report the incident to regulators and customers and may have to face lawsuits. The reputational damage can trigger a customer's distrust that may take years to recover from. This is what happens when security is not embedded from day one. Even a single misconfigured or unencrypted data transfer becomes a vulnerability.

➡️ Fraud & Unauthorized Access

Worried about stolen cards and forged signatures? Financial fraud has evolved far beyond that. Attackers use different methods, such as synthetic identity fraud, social engineering for unauthorized access to payment and banking systems, and account takeover attacks.

The main problem is the authentication architecture. Systems that lack strong identity checks at every access point, including transaction approvals, login, API calls, and admin access, develop gaps that the fraudsters could actively exploit. Multi-factor authentication and continuous session monitoring are now architectural requirements.

➡️ API Vulnerabilities

Modern BFSI systems are API-backed, which makes them powerful yet exposed. When APIs are poorly secured, they become one of the most exploited attack vectors in financial services. Excessive data exposure, missing input validation, broken authentication, and a lack of rate limiting can allow attackers to fetch data or bypass business logic.

Open Banking regulations have expanded API surface areas, which makes API security a first-class architectural concern and not an afterthought.

➡️ Insider Threats

Not every threat comes from outside of the organization, sometimes the threat can be among us. It could be employees, system administrators, contractors, or someone with privileged access. Insider threats can be malicious for several reasons.

A security-first architecture addresses the issue through the principle of least privilege, meaning every user, service, and system component is granted the minimum access required to perform its function. With the help of audit logging and real-time access monitoring, any unusual access pattern can be detected before they escalate.

➡️ Third-Party Integration Risks

Financial institutions increasingly depend on third-party platforms for analytics, payments, compliance checks, credit scoring, cloud services, and digital customer experience. And each of these integrations creates dependencies.

If integration lacks proper isolation and monitoring, a mere vulnerability in a third-party system can propagate into the bank's core infrastructure. Security-first architecture mandates rigorous third-party risk assessment, sandboxed integration layers, and API gateway controls before any external system is connected.

The Business Impact of Security Failures in BFSI

In financial services, the moment a breach happens, it doesn't stay confined, it affects customer data, transactions, or compliance obligations, and it becomes a business problem. This is why security in BFSI cannot be viewed as a technical safeguard, but affects trust, operations, and business stability.

🔷 Financial Loss

A security breach can create major financial damage.

- Fraudulent transactions

- Forensic investigations

- Recovery costs

- Legal expenses

- Emergency remediation

All of it can quickly add up. And in many cases, the cost of responding to a breach is far more than preventing it.

For BFSI, enterprise software development for banking can prove to be highly beneficial.

🔷 Regulatory Penalties

As you know, financial businesses function under strict regulatory frameworks. In such a case, if a platform fails to safeguard sensitive customer data, meet security compliance requirements, or maintain an audit trail, it could result in substantial fines and legal scrutiny.

Apart from the penalty, breaches can slow down operations and delay transformations, increasing future compliance costs.

🔷 Reputation Damage

Trust is the product in financial services, and customers entrust their bank with their life savings. But once that trust is broken, recovery is tough. Even a single public security issue can lead to customer churn, long-term brand damage, and loss of investors. The reputational cost of a security failure in BFSI takes years to fix, not weeks.

🔷 Operational Disruption

Security incidents in BFSI disrupt business continuity. Ransomware attacks or compromised specific banking systems can stall transaction processing, freeze customer access, and suspend important financial operations for hours. In this sector, where real-time services and downtime are barely tolerated, even a minor disruption can create a major impact.

All of this comes down to security not being an IT risk, but a business risk.

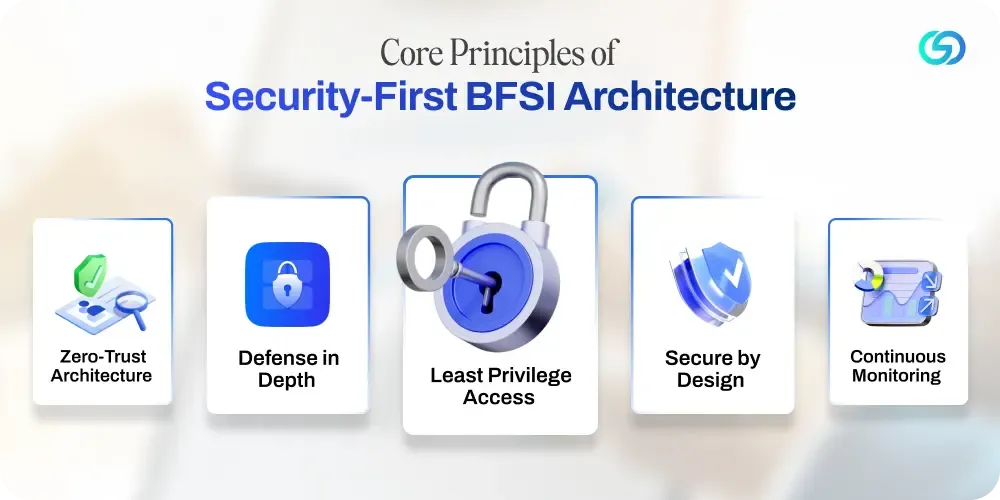

The Core Principles Behind Security-First BFSI Architecture

Not a single technology or tool, security-first architecture is a set of foundational principles that govern how BFSI systems are developed and operated.

Here are the main principles that make security-first architecture work in modern BFSI systems.

1️⃣ Zero-Trust Architecture

Trust cannot be assumed in finance. Every device, app, user, and API request needs to be verified, whether it comes from outside the organization or within.

What this means in practice:

- Every login request is authenticated

- Session trust is continuously re-evaluated

- Every API call is validated

Why it matters in BFSI:

A user inside the network should be safe. Continuous authentication reduces the risk of compromised credentials and unauthorized internal access.

2️⃣ Defense in Depth

Depending on one security control is risky. A strong approach is to develop multiple layers of protection so that if one control fails, another layer continues protecting the system.

Typical layers include:

- Network security controls

- Endpoint security

- Application-level protection

- Encryption

- Monitoring and alerting system

Why it matters in BFSI:

Enterprise banking software manages high-value transactions. Multi-layered security reduces the chance of one vulnerability exposing the entire system.

3️⃣ Least Privilege Access

Not every system or third-party service needs access to everything. Access should be granted only to the resources required.

- A secure access model usually includes:

- Role-based access control (RBAC)

- Permission segregation

- Temporary elevated access when required

- Regular access reviews

Why it matters in BFSI:

Minimal access limits the impact of insider threats, compromised accounts, and accidental misuse of sensitive financial data.

4️⃣ Secure by Design

One of the common mistakes is treating security as a testing-stage activity. Security-first organizations do the opposite. They start asking questions right from the planning stage:

- What sensitive data can this system handle?

- Which APIs will be exposed?

- What are the compliance requirements?

Why it matters in BFSI:

When security is built into your architecture, systems become stronger and easier to govern.

5️⃣ Continuous Monitoring

A secure system is not one that was tested once, but it is through continuous monitoring, teams can detect unusual activity the moment it happens.

Continuous monitoring covers:

- Real-time threat detection across all system layers

- Automated suspicious login alerts

- Audit trails that satisfy regulatory requirements

- API misuse monitoring

Why it matters in BFSI:

Security monitoring is not limited to just compliance activities, but enterprise software development for banking protects revenue and customers every day.

This is how the principles work in sync:

- Zero trust: Who is allowed in?

- Defense in depth: What happens when one control fails?

- Least privilege: How much damage can a breach cause?

- Secure by design: Was security built in from the initial day?

- Continuous monitoring: Are we detecting threats in real-time?

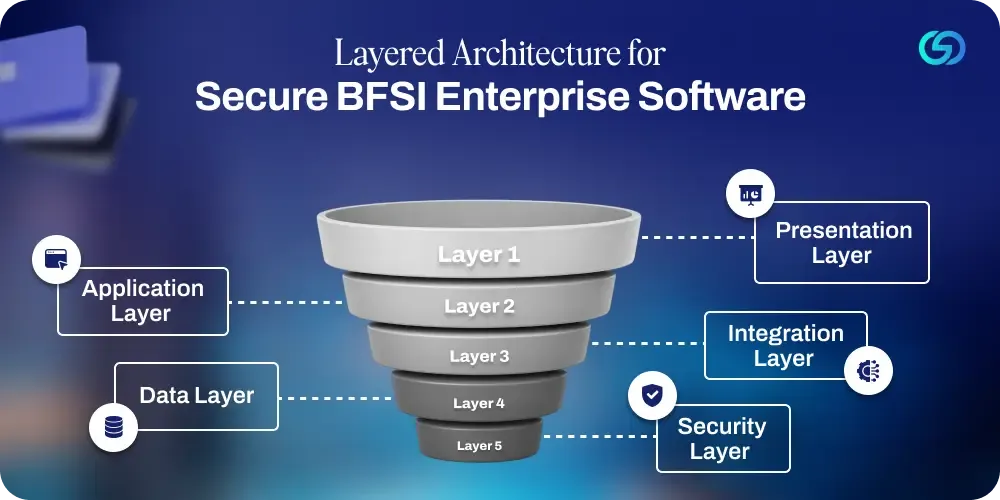

Enterprise BFSI Architecture: The Layered Foundation of Secure Financial Software

Banks and financial services operate in a landscape that is heavily regulated and diverse. Quick changes in fintech partnerships, open banking, or changing cybersecurity threats require a deep understanding of the way data, systems, and processes interconnect.

Enterprise architecture gives a picture of the whole operating model- the people, processes, technologies, and information all in one place.

In enterprise banking software, architecture isn't just a blueprint, but it completely determines how securely and efficiently financial services work. A modern enterprise banking software platform is designed as a layered architecture in which each layer plays a distinct role.

⏺️ Layer 1: Presentation Layer

This is where both customers and users interact through web applications, internal dashboards, and mobile banking apps. BFSI enterprise software development for banking provides you with a user-friendly platform that ensures every element is built with security.

- Secure UI/UX design: Session timeout controls, anti-phishing interface patterns

- Web & mobile apps: Built to OWASP standards, preventing vulnerabilities at the front end

- SSL/TLS enforcement: All data exchanged between systems and a user is encrypted

A well-secured presentation layer in a banking platform prevents attackers from entering.

⏺️ Layer 2: Application Layer

Think of it as an operational engine for your platform. The application layer is where most businesses are executed, and financial decisions are made.

Key components at this layer include:

- Business logic engines: Loan eligibility calculations, insurance underwriting, interest processing

- Microservices architecture: Payments, KYC notifications, etc., allow secure updates without system-wide disruption

- Service-to-service authentication: Internal service call is authenticated

For BFSI software development, this layer is where speed and performance come together.

⏺️ Layer 3: Integration Layer

Enterprise banking software doesn't function in monoliths, but connects with payment networks, KYC platforms, third-party fintech providers, and cloud services. The integration layer handles all of this connectivity, and it is also said to be the highest-risk layer in the entire architecture.

Critical components include:

- API gateways: A centralized point for all inbound and outbound API traffic.

- Middleware: Manages data transformation, message routing, and protocol translation

- Third-party integration sandboxing: External connections are isolated and monitored to prevent vulnerabilities from reaching core banking systems

Don't let an unsecure integration layer become the root cause of data breaches. Every point of connection is a potential attack surface.

⏺️ Layer 4: Data Layer

Data is the real asset in BFSI. Financial records, transaction histories, insurance data, credit profiles, and compliance documentation are to be stored and transmitted with a high level of protection.

This is what the data layer in the security-first BFSI architecture includes:

- Relational databases: For transaction data requiring strict consistencies

- Data lakes & warehouses: For analytics, AI model training, and fraud pattern analysis

- Data residency compliance: Multinational BFSI companies need data to be stored in a way that complies with local regulatory guidelines

- Backup and disaster recovery: Automated and encrypted backups ensuring continuity under any failure scenario

This layer ensures financial data resumes secure and available because in BFSI, losing data integrity means losing operational trust.

⏺️ Layer 5: Security Layer

This is exactly what differentiates a security-first architecture from a standard one. The security layer operates across every other layer simultaneously. There are three core pillars that make up this layer:

- Identity & Access Management (IAM): For controlling who can access what

- Encryption: For safeguarding data in transit and at rest

- Monitoring & threat detection: For recognizing suspicious activity in real-time

Enterprise banking software development company ensures that this security layer is what turns basic software into a robust, enterprise-ready system.

Which Security Components Make or Break a BFSI Software System?

Security in BFSI software development is only as strong as the components built into the system's architecture. The key security components in BFSI systems are designed to maintain trust, protect sensitive data, and comply with strict regulations. A robust security relies on a multi-layered approach. Let's go through the key components:

⏩ Identity & Access Management (IAM)

IAM ensures only verified users and systems can access sensitive banking resources.

- Multi-factor authentication: Adds a mandatory second verification layer

- Role-based access control: Assigns system permissions strictly

⏩ Encryption

Encrypted systems ensure sensitive financial data remains unreadable.

- Data at rest: All stored data of customers and transactions is encrypted

- Data in transit: Encrypts every data exchange between users, systems, and services

⏩ API Security

In BFSI systems, deeply connected third-party platforms, payment, and unsecured APIs are one of the most exploited attack vectors.

- OAuth 2.0 & JWT: Secure authentication method that validates apps, users, and API requests

- Rate limiting: Blocks excessive API requests to reduce abuse and service overload

⏩ Threat Detection Systems

Financial institutions spot suspicious behavior before it transforms into fraud or disruption with threat detection systems.

- Security information and event management: Analyzes security events across the platform in real-time

- AI-powered fraud detection: Detects unusual transaction patterns, anomalies, and potential fraud attempts

⏩ Audit & Logging

Every action within a BFSI system should be recorded and audit-ready, both for internal governance and regulatory compliance.

- Compliance tracking: Maintains a traceable record to support audits, reporting, and regulatory compliance requirements.

- Activity logs: Records user actions, access attempts, and system changes for investigation and accountability.

Secure Software Development Lifecycle (SSDLC) in BFSI

SSDLC is a software development lifecycle concept that focuses on a secure product. This approach requires security testing at all stages of software development, right from planning to implementation.

The SSDLC process can be divided into six phases. Let’s take a closer look at them.

🔷 Phase 1: Requirements

- Define data protection needs for customer and transaction information

- Analyze regulatory needs such as AML, KYC, PCI-DSS, or GDPR

🔷 Phase 2: Design

- Perform threat modeling to recognize possible paths for attacks

- Design secure data flows, access controls, and integration boundaries

🔷 Phase 3: Development

Follow secure coding practices to eliminate the risk of injection flaws and insecure authentication

Leverage code reviews and security checks during development

🔷 Phase 4: Testing

- Perform penetration testing to simulate real-world attack scenarios

- Run vulnerability scans to check weaknesses in codebase and libraries

🔷 Phase 5: Deployment

- Use secure CI/CD pipelines to enforce automated security gates, ensuring no build reaches production without undergoing security checks

- Ensure credentials and configurations are protected during release

🔷 Phase 6: Continuous Maintenance

- Continuously monitor system behavior, threat signals, and access patterns in real-time

- Regular security patches and periodic re-assessments ensure that the system remains safe even though the threats evolve

In enterprise banking software, security isn’t a one-time thing, rather it’s a continuous process.

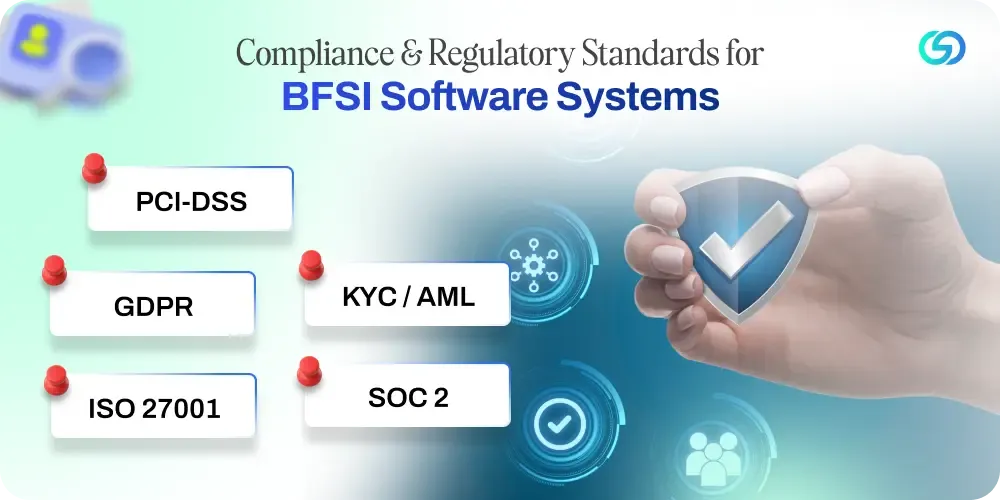

Compliance & Regulatory Frameworks Every BFSI System Must Meet

Regulatory compliance is non-negotiable in BFSI that promotes transparency, customer protection, and risk management.

Sure, regulatory compliance is complex for financial businesses as they navigate through the evolving regulations and increasing expectations around transparency and real-time monitoring.

According to research, nearly 98% of financial services organizations reported increased financial crime compliance costs, totaling approximately $61 billion annually across the US and Canada. Failure to maintain BFSI compliance can cause severe financial and reputational damage that causes long-term growth.

Here are global compliance frameworks:

➡️ PCI-DSS: It governs how financial systems handle cardholder data, requiring secure payment processing, strict access controls, encryption, and active monitoring to reduce the risk of fraud across banking ecosystems.

➡️ GDPR: For any BFSI institution operating in the European Union, GDPR compliance outlines how personal data is collected, stored, and deleted. This influences customer onboarding systems, analytics tools, account management platforms, and other systems that handle Personally Identifiable Information (PII).

➡️ KYC / AML: KYC and AML regulations remain at the center of modern financial operations. These frameworks need to verify customer identities, detect suspicious activities, and monitor transactions. It means compliance is deeply connected to system design.

➡️ ISO 27001: It is a globally recognized standard for maintaining an Information Security Management System (ISMS). ISO 27001 goes beyond regular-specific frameworks, covering the entire security posture—spanning people, technologies, and processes.

➡️ SOC 2: It focuses on the extent to which organizations protect customer data through internal controls. SOC 2 ensures security, availability, and confidentiality, helping financially demonstrate trustworthiness to clients and partners.

Integration Challenges and Solutions in BFSI Systems

It’s no secret, but integrations are seen to be a key challenge for the banks today. We have surely come a long way in the finance and banking domain, however, many financial institutions are still running on core banking systems that were built some decades ago.

▶️ Legacy Core Banking Systems

The challenge:

Most banking systems weren’t designed for today’s digital speed, and connecting them with advanced apps and real-time services can only become messy.

The solution:

Middleware and a secure integration layer allow old systems to communicate with new platforms without hampering the daily banking operations.

▶️ Third-Party Fintech Integrations

The challenge:

Every third-party connection, like payment gateways, brings vulnerabilities into your existing ecosystem. In banking software, even one weak external link can compromise the core operations.

The solution:

The safest approach is controlling isolation, meaning isolating every external connection from the core systems. Secure integration layers monitor third-party connections, validate them, and separate them from internal banking systems.

▶️ API Exposure Risks

The challenge:

Data leaks, traffic abuse, and unauthorized access can happen when APIs are poorly protected.

The solution:

An API gateway is a single-entry point for all API traffic. It enforces authentication, applies rate limiting, and logs every interaction. In enterprise software development for banking, an API gateway is crucial for integration security.

▶️ Data Synchronization Issues

The challenge:

Certain data, such as, transactions, compliance logs, and customer records live across different systems and updates at different speeds. But, when they fall out of sync, the outcomes can range from duplicate transactions to failed audits.

The solution:

Secure integration layers ensure that every system update is synced in real-time. This helps in maintaining a single source of truth across the ecosystem and removes inconsistencies as well.

How AI and Automation Are Transforming BFSI Security

AI is here, and we are witnessing a major structural shift today with AI and automation running essential industries. For example, JPMorgan Chase’s AI system processes would only require 360,000 hours for lawyers to review and analyze 12,000 agreements with utmost accuracy, decreasing the risk of operational overhead.

Between 2024 and 2029, AI in the BFSI sector is estimated to grow $101.35 billion, which is a significant shift in how BFSI providers run operational support.

🔶 Fraud Detection

Real-time identification of odd transaction patterns and fraud across payment channels.

- Behavioral pattern recognition

- Real-time transaction monitoring

- Adaptive fraud prevention

How ConvexSol helps:

ConvexSol helps build AI-powered fraud detection engines that integrate into payment and core banking systems. This helps in real-time decision-making with self-improving models that adapt as fraud patterns evolve.

🔶 Risk Scoring

Assigns real-time risk scores to users, transactions, and activities before approval decisions are made.

- Transaction risk assessment

- Dynamic decision-making driven by risk thresholds

- Device, location, and usage pattern analysis

How ConvexSol helps:

ConvexSol combines AI, RPA, and automation to build real-time risk scoring capabilities into financial workflows. AI analyzes transaction and behavioral signals, on the other hand, automation triggers instant approvals or escalations based on defined thresholds.

🔶 Behavioral Analytics

Learns normal user behavior and detects unusual activity that may indicate compromised accounts, insider misuse, or suspicious access attempts.

- User behavior baselining

- Login and access anomaly detection

- Pattern deviation alerts in real time

How ConvexSol helps:

ConvexSol enables behavioral intelligence capabilities within modern BFSI software development environments. By analyzing access patterns and transaction behavior continuously, institutions can identify suspicious activities early on and respond before it escalates.

🔶 Automated Compliance Checks

AI helps automate repetitive tasks regarding compliance monitoring, which, in turn, helps remain consistent and audit-ready across the operation.

- Automated rule-based transaction screening

- Suspicious activity flagging in real-time

- Speedy compliance validation and reporting

How ConvexSol helps:

With the help of AI, RPA, and automation, ConvexSol simplifies compliance-heavy operations. AI detects suspicious activities, RPA manages the repetitive validation tasks, and automation allows for faster screening and audit-ready compliance monitoring.

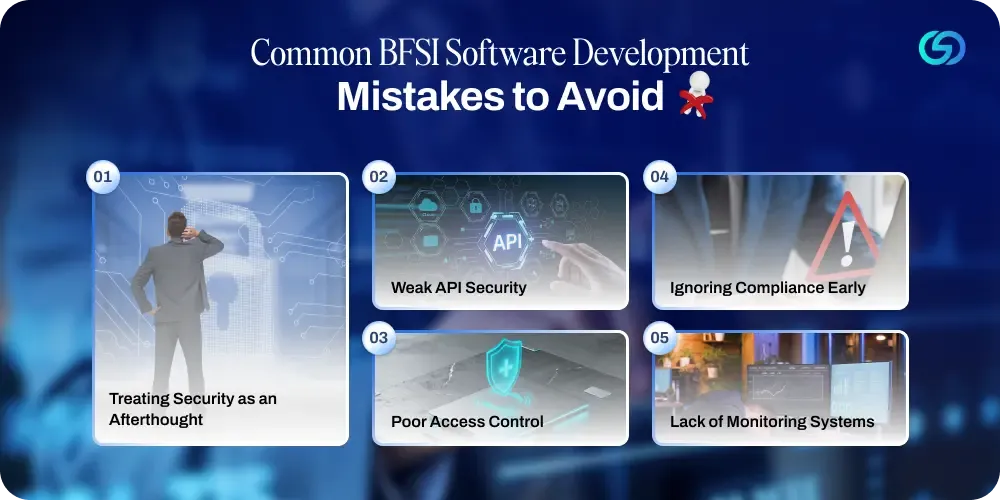

Common Mistakes of BFSI Software Development

Like many other industries, the dynamic nature of finance leads to unique challenges in the software development sphere. Although the issues are not unique, however, their impact becomes apparent with time as financial systems become too intricate.

Knowing and addressing the mistakes of BFSI software development is crucial in shaping the future of this sector.

*️⃣ Treating Security as an Afterthought

What happens?

You build a platform, integrate the features, and eventually, users onboard too. Somewhere near the launch, you realize, “What about security?

At this point, security is not a design decision anymore. Fitting security into a live BFSI platform means system downtime, architectural rework, and compliance gaps.

The cost?

Higher remediation costs, delayed go-live, and a system that is less secure.

*️⃣ Weak API Security

What happens?

APIs are built quickly and are minimally secured. Authentication is inconsistent, and legacy endpoints that nobody remembers still exist and continue to function.

In a connected BFSI ecosystem, a poorly secured API endpoint is all an attacker needs.

The cost?

Data exposure, unauthorized access to transactions, and financial losses following public API breaches in financial services.

*️⃣ Poor Access Control

What happens?

Permissions are assigned during development for convenience and not reviewed after going live.

Developers retain production access, vendors have broader data visibility, and former employees exist in the system longer than they should.

The cost?

Insider threat becomes easier to execute, the impact of breaches grows larger, and audit findings increase.

*️⃣ Ignoring Compliance Early

What happens?

Compliance obligations are treated as a pre-launch checklist. The system is built, evaluated against regulatory requirements, and if gaps are found, rework begins.

This is one of the common BFSI software development mistakes.

The cost?

Expensive architectural rework, delayed launches, and regulatory penalties caused by systems going live without meeting compliance requirements.

*️⃣ Lack of Monitoring Systems

What happens?

A platform will fail to respond to threats it cannot see.

Suspicious patterns, fraud attempts, or unusual system behavior go unnoticed until damage is already done.

The cost?

A contained incident turns into a major breach, and regulatory penalties increase every day as the threat remains undetected.

Cost of Security vs Cost of a Breach

Most managers have asked this question: “Do we really need to spend this much on security?”

Security investment in BFSI feels like a huge number until you put it against the cost of breach.

Let’s understand the difference between the cost of security vs cost of a breach.

| Factor | Investing in Security-First BFSI Architecture | Cost of a Security Breach |

|---|---|---|

| Initial investment | Planned investment in secure architecture, compliance, encryption, and monitoring systems | Unplanned emergency spending on remediation, recovery, and legal support |

| Financial Impact | Long-term security budgeting | Direct financial losses, regulatory fines, and fraud exposure |

| Business Continuity | Stable operations with lesser disruption risk | Transaction failures, service downtime |

| Customer Trust | Develops confidence in digital banking and financial platforms | Loss of customer trust and reputational damage |

| Compliance Readiness | Audit preparation is easier and ensured regulatory alignment | Failed audits, penalties, and compliance risks |

| Response Time | Faster threat detection | Delayed detection leading to larger damage |

| Long-Term ROI | Lower recovery costs | High recovery expenses |

| Scalability | Secure for future digital transformation and integrations | Security gaps become larger and expensive as systems grow |

| Competitive Advantage | Stronger market credibility | Negative publicity affecting business growth |

Your Step-by-Step Roadmap to Security-First BFSI Architecture

In enterprise banking software for BFSI, security cannot be treated separately. It has to be planned, tested, and improved continuously throughout the entire lifecycle of the system.

For the BFSI industry, a security-first approach creates a stronger protection against cyber threats, building compliance readiness and customer trust.

Here’s a practical roadmap financial institution must follow for a secure ecosystem.

💠 Step 1: Assess Current Systems

Begin with a detailed review of every application, data flow, and infrastructure component. Documenting existing security controls and integration points builds a complete architectural baseline before anything else.

💠 Step 2: Identify Vulnerabilities

Spot weaknesses across applications, APIs, and automated vulnerability scans across all layers. The result is a prioritized list of risks based on their seriousness and business impact, not just a mere list of issues.

💠 Step 3: Define Security Architecture

You should document zero-trust models, IAM requirements, and API governance before development begins. Make sure to map compliance requirements for specific architectural control.

💠 Step 4: Implement IAM & Encryption

Safe financial systems use robust identity governance, encryption mechanisms, and controlled access permissions to secure sensitive customer and transaction data across the enterprise ecosystem.

💠 Step 5: Secure APIs & Integrations

Modern enterprise banking software depends on APIs and external integrations, enforcing OAuth 2.0, JWT, rate limiting and more for securing every endpoint. Legacy APIs should be reviewed regularly, and every integration must pass strict security validation before deployment.

💠 Step 6: Enable Monitoring Systems

Across all system layers, configure SIEM, AI-driven threat detection, and real-time alerting. Clear incident response and regulatory notification of workflows, so teams know how to respond when threats are found.

💠 Step 7: Ensure Compliance

Validate every compliance requirement against a particular security or architectural control. Fix the gaps, if any, with targeted improvements instead of developing systems because compliance was built into the design from the start.

💠 Step 8: Continuously Improve

Security in BFSI is an ongoing process that requires regular testing, updates, monitoring, and optimization to adapt to the changing cyber threats and regulatory expectations. It is how you remain secure for the long-term.

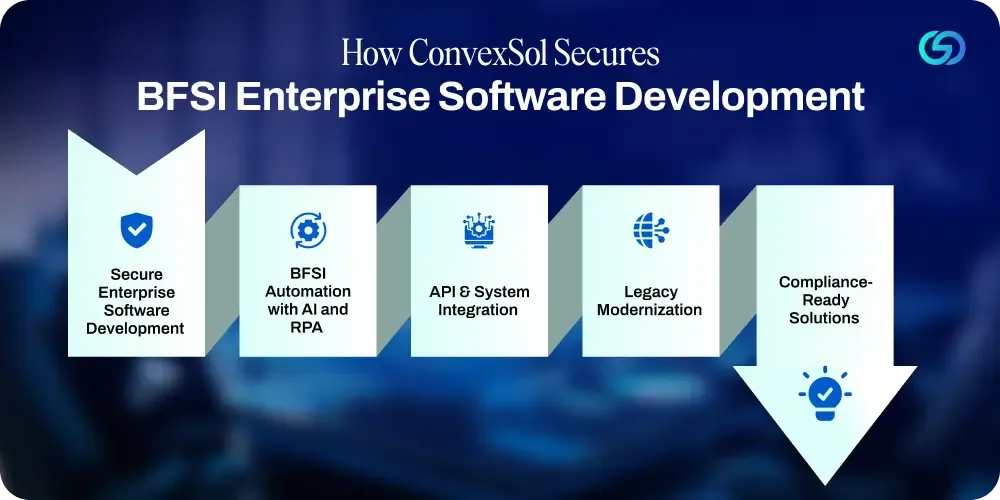

How ConvexSol Strengthens Enterprise Software Development for BFSI

As a specialized BFSI software development company, ConvexSol partners with banks, lending platforms, insurance companies, and financial facilities to modernize enterprise systems, where security stands as the pillar.

➡️ Secure Enterprise Software Development

Every platform ConvexSol builds is designed with Zero-Trust principles, compliance frameworks, and defense-in-depth embedded into your system from day one.

➡️ BFSI Automation with AI and RPA

Manual processes in BFSI mean inviting risks. Our team of experts help automate fraud monitoring, compliance work, decision-heavy processes, and repetitive operational tasks using AI and RPA. The result is faster and more automated while satisfying regulatory requirements.

➡️ API & System Integration

Modern BFSI enterprises run on connectivity. Every connection point is risky if not governed accurately. We design and implement secure integration architecture that connects complex ecosystems without exposing them. Each integration is monitored, ensuring third-party connectivity doesn’t become a liability.

➡️ Legacy Modernization

Our professionals help financial businesses modernize infrastructure without causing disruption to the workflow that makes the older system more secure and integration ready.

➡️ Compliance-Ready Solutions

Compliance shouldn’t slow down innovation. We develop enterprise banking software with compliance built-in from the very start. Whether it is access to governance, audit trails, or secure data handling, BFSI enterprises stay ready for changing regulatory needs without adding intricacies later on.

Frequently Asked Questions

How do I know if my current BFSI software needs modernization?

If your team is spending time managing system limitations rather than improving customer experience, it’s a sign that modernization is overdue. Slow integrations, security gaps, rising maintenance expenses, and failing to adapt to compliance changes are some of the biggest indicators.

How often should the security-first framework be reviewed?

In BFSI, reviewing security shouldn’t be an annual activity. Access control, integrations, architectures, and compliance policies need continuous reviewing with deeper analysis conducted with the introduction of new integrations or digital services.

Do you offer security audits for systems already in production?

Yes, we do. ConvexSol helps BFSI enterprises assess live systems for architectural weaknesses, compliance gaps, access control issues, and integration of vulnerabilities. The goal is not to spot risks but to see what impacts business continuity.

Does ConvexSol offer post-deployment support and maintenance?

Yes. In BFSI environments, deployment is just the beginning. At ConvexSol, we offer ongoing support that includes security optimization, continuous monitoring, performance improvements and more as regulatory needs evolve.